New Integrated Shield Plan (IP) Riders

In compliance with the revised requirements announced by MOH in November 2025

Last updated 1 April 2026

New rider requirements from 1 April 2026

MOH introduced new requirements for Integrated Shield Plan (IP) riders to address rising insurance premiums and private healthcare costs.

All seven IP insurers have launched new rider products. On average, premiums of new IP riders (with maximum coverage) are around 35-40% lower than those of legacy riders.

Review and right-size your rider coverage

While we value private health insurance for peace of mind and the autonomy to choose our preferred healthcare options, it is important to ensure that our private health insurance coverage is right-sized to our healthcare needs and long-term finances. Click the links to understand your options.

Learn about Singapore’s healthcare financing framework

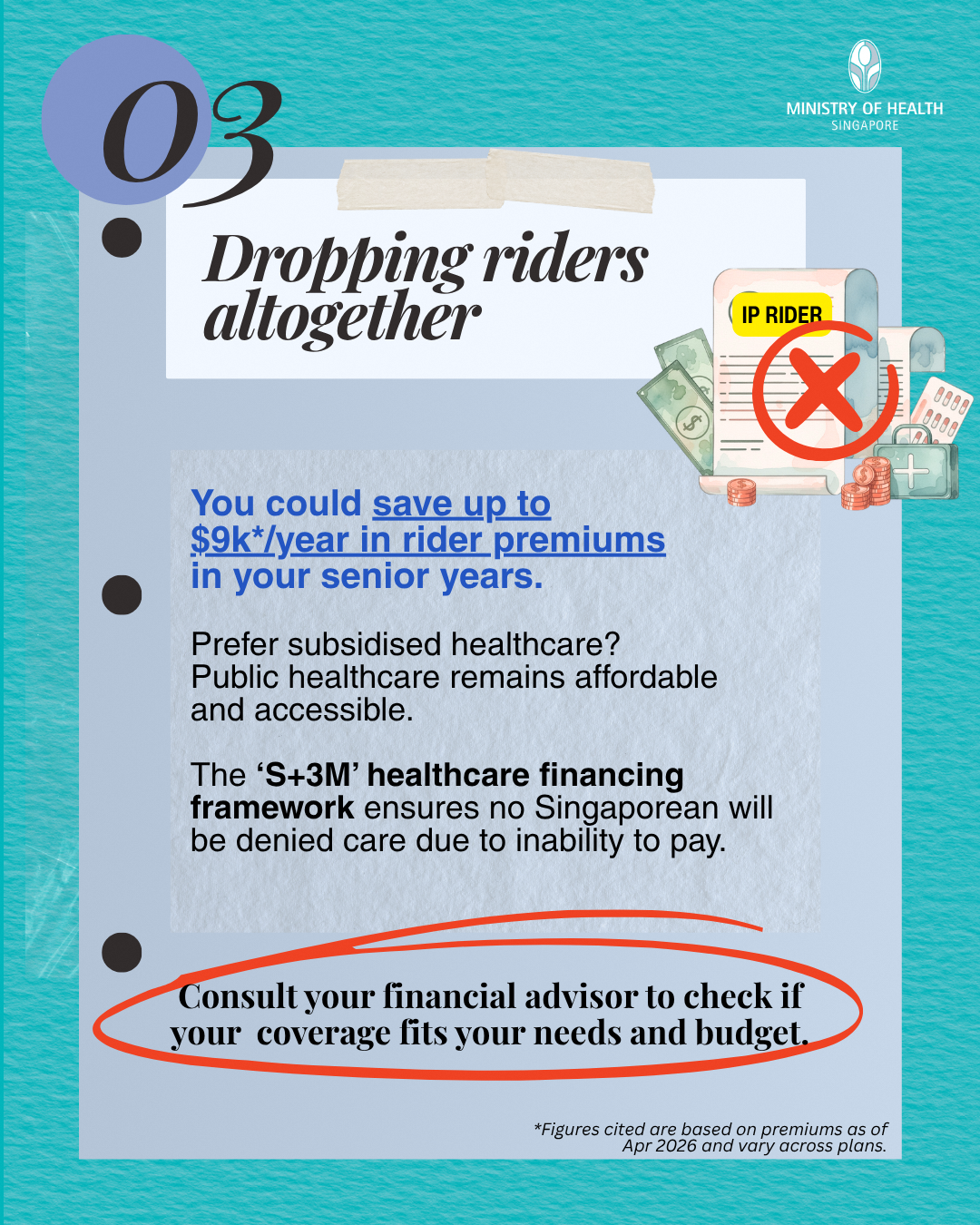

With S+3Ms, public healthcare remains affordable and accessible to all Singaporeans. No Singaporean is denied appropriate care due to inability to pay. Learn more about S+3Ms here.

S+3Ms explained

Ensuring the sustainability of private healthcare

Prefer unsubsidised healthcare? You can consider buying additional private insurance coverage, such as Integrated Shield Plan (IP) and riders.

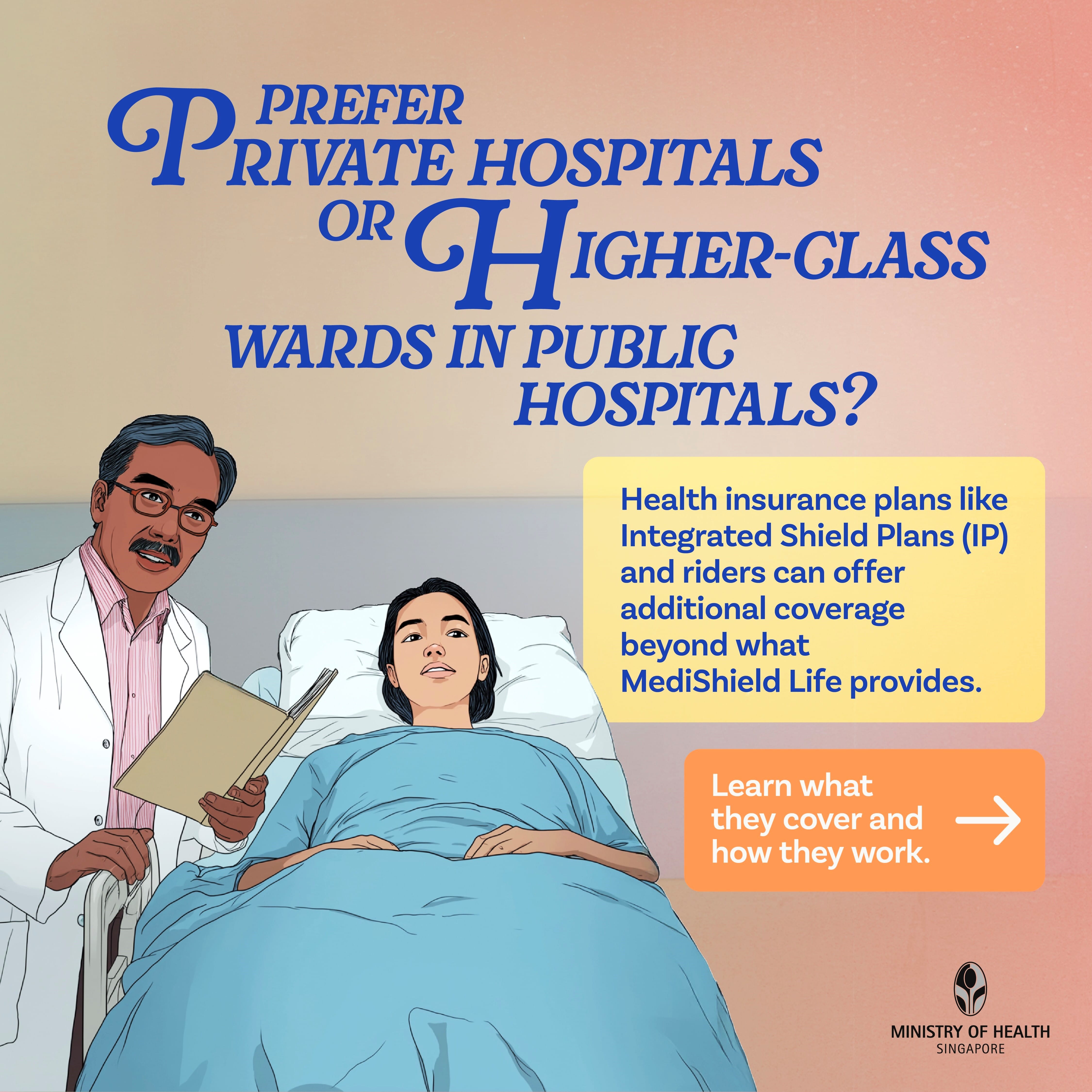

Role of IP

IP provides additional coverage on top of MediShield Life, to cover private wards and private healthcare institutions. They are offered by private insurers, and are optional. IPs are useful if you intend to seek medical care at higher-class wards in public hospitals, private hospitals, or prefer to choose your own doctor.

Learn more about how IPs work here and compare your options here.

Role of riders

Riders are optional add-ons for your IPs, to help reduce cash co-payment upon admission. They have varying levels of coverage, depending on your needs and budget. Rider premiums must be fully paid in cash, and they increase significantly as you age, and cost more than IPs.

Understanding how IP and riders work

Choosing the right level of health insurance coverage

Riders are meant to protect you from large medical bills by reducing the out-of-pocket expenses to a manageable amount. However, is paying higher premiums worth the extra protection overtime?

Today, many Singaporeans may be paying more premiums than they need to, especially for riders. Choose the right level of private insurance coverage based on your needs and long-term affordability.

Use the Health Insurance Planner to find out how much you've been paying for health insurance, and consult your financial advisor to find out more.

Uncover the myths and value of IP riders

Loosening the private healthcare financing ‘knot’

The new requirements for IP riders are part of MOH’s efforts to put private healthcare and private health insurance on a more sustainable path.

Generous coverage from IP riders has contributed to a greater tendency for over-servicing and over-consumption of healthcare services, resulting in rising claims, and in turn rising rider premiums. Our private healthcare financing system is therefore in a ‘knot’.

To loosen the ‘knot’, MOH is working with stakeholders to address these underlying issues and moderate healthcare cost increases.

As healthcare consumers, we can help to loosen the ‘knot’ by buying the right level of insurance coverage based on your needs and long-term affordability.